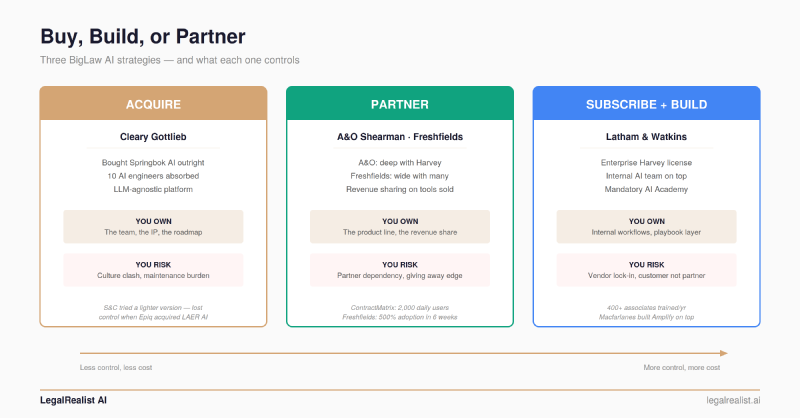

Buy, Build, or Partner: Three BigLaw Bets on AI#

TL;DR

- A&O Shearman turned institutional knowledge into recurring revenue. ContractMatrix and agentic tools built with Harvey are sold to other firms on subscription. Freshfields took the same approach with multiple partners — Google, Anthropic, and Thomson Reuters simultaneously.

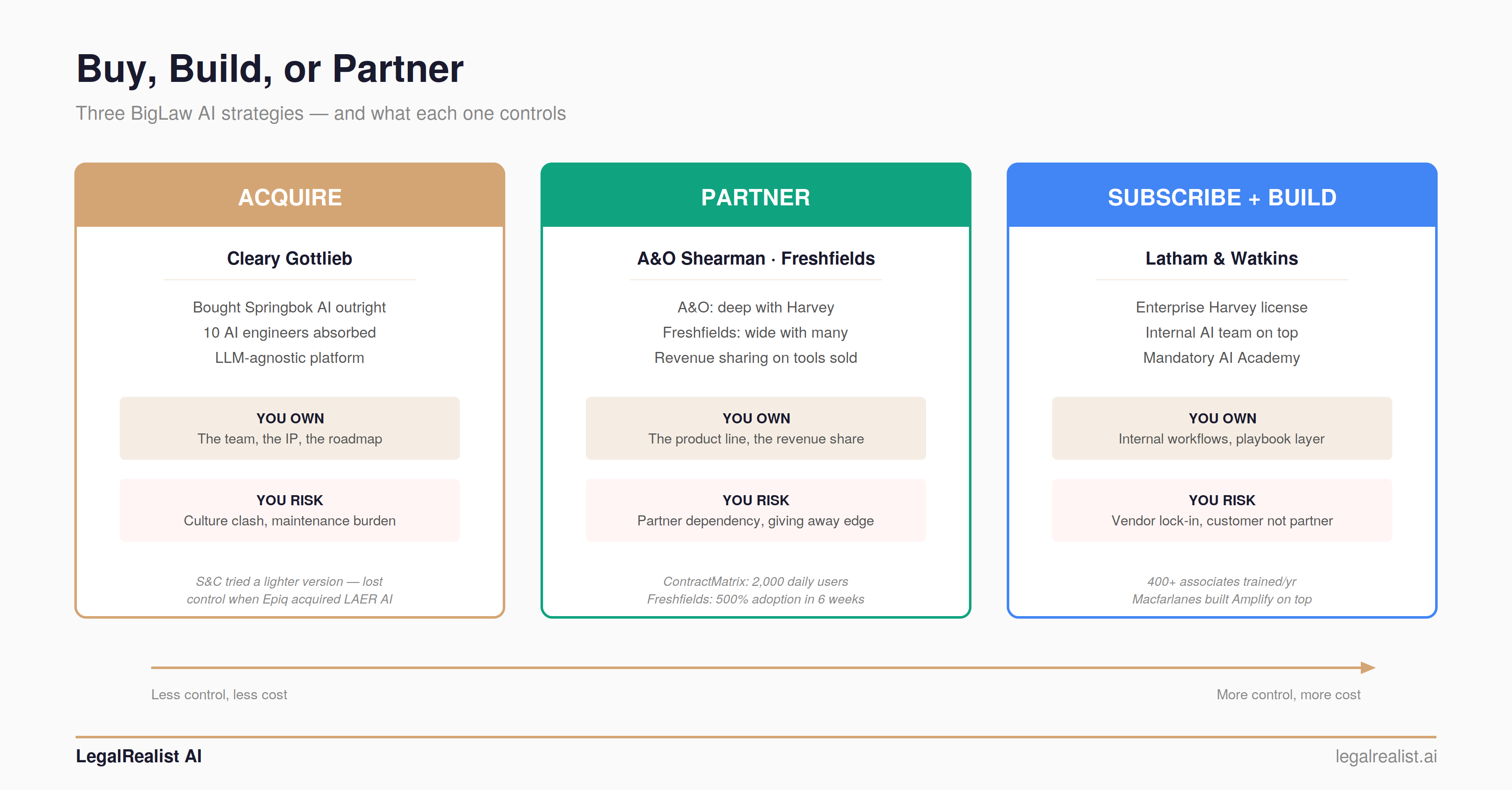

- Cleary acquired a team, not just a tool. Absorbing Springbok’s 10 AI engineers solved the talent problem that individual hiring can’t — but the acquisition is over a year old with no published adoption metrics. S&C’s lighter-touch investment in a startup shows why deal structure matters: when the startup was acquired, the technology walked out the door.

- Latham’s subscribe-and-build model is the one most firms will follow. An enterprise Harvey license for general capabilities, an internal AI team for firm-specific workflows, and a mandatory AI Academy that trains 400+ associates per year with billable credit.

- Structure your arrangement to match your risk tolerance. An acquisition gives you control but not scale. A co-development partnership gives you both — if the partner stays aligned. A platform subscription gives you speed — but you’re a customer, not a partner.

- These bets aren’t mutually exclusive — place more than one. Even Cleary, the clearest “acquire” example, runs a third-party platform firmwide too. Treat the three strategies as a menu to mix by workflow, not a single doctrine to commit to.

Corrections & Updates

- June 13, 2026: Added Harvey’s March 2026 funding round ($200M at an $11B valuation) and its May 2026 expansion into the institutional-knowledge layer (the Command Center and DeepJudge partnership) to the partner-dependency and subscribe-and-build sections.

When Cleary Gottlieb acquired a London AI startup in March 2025, the ABA Journal called it an “extremely rare” move. Law firms license technology. They don’t buy technology companies. But across the Atlantic, A&O Shearman had already gone further — co-developing AI tools with Harvey and negotiating a revenue-sharing deal to sell those tools to other law firms. Latham & Watkins took a different path: an enterprise Harvey license for the platform, then an internal team building firm-specific workflows on top — the subscribe-and-build model that more firms are likely to follow.

Three strategies, one question: who controls the AI your lawyers rely on?

Buy the Whole Company#

In March 2025, Cleary Gottlieb did something almost no BigLaw firm had done before: it acquired a technology company outright. Springbok AI, a London-based generative AI product development firm founded in 2017, had previously built tools for Dentons, Hogan Lovells, and EY. Cleary didn’t just license the product — it absorbed the entire operation: the proprietary SpringLaw platform, co-founder and CEO Victoria Albrecht, and a team of 10 data scientists and AI engineers.

The Springbok team became Cleary’s AI Acceleration team, embedded directly within the firm to build custom tools for practices that benefit from summarization, data extraction, and workflow automation. It is led by Springbok co-founder and CEO Victoria Albrecht and works alongside two existing innovation arms: the e-Discovery and Litigation Technology (DLT) group and ClearyX, the firm’s alternative legal services operation launched in 2022. The Director of Practice Innovation who originally oversaw the group, Ilona Logvinova, left Cleary in November 2025 to become Chief AI Officer at HSF Kramer. (These three strategies are illustrative, not mutually exclusive: Cleary also subscribes to the third-party platform Legora firmwide, announced May 2025 — even the clearest “acquire” example runs a buy-and-subscribe hybrid.)

Managing Partner Michael Gerstenzang has been one of the more vocal BigLaw leaders on the subject of AI adoption. He told Bloomberg Law that generative AI could help firms move away from the billable hour and reduce the structural advantage of brute-force staffing. The Springbok acquisition was the operational follow-through on that thesis.

Control. The Springbok team works exclusively for Cleary. Its tools are purpose-built for the firm’s practice areas and clients. When a model provider ships an update that breaks a prompt, Cleary has in-house engineers who can fix it the same day — they don’t wait in a vendor’s support queue. SpringLaw is LLM-agnostic, meaning the firm isn’t locked into any single model provider.

Talent. Recruiting data scientists and AI engineers is brutally competitive. Acquiring a team of 10 with legal-domain experience is faster and more reliable than hiring them individually, especially when you’re competing against tech companies paying equity compensation that law firms can’t match.

But the acquisition carries real risks. Technologists and lawyers operate in different cultures with different incentive structures, and the talent an acquisition secures can still leave — Cleary’s senior innovation leader departed for a competitor within a year of the deal. If the AI Acceleration team can’t build tools lawyers actually use on live matters — not demos that impress at retreats — the acquisition becomes an expensive internal consultancy. A team of 10 is enough to build initial tools, but maintaining them across practice groups while keeping pace with competitors who have hundreds of engineers requires sustained investment. And Cleary’s tools are built for Cleary — they don’t have the feedback loop of a product company serving hundreds of firms. The acquisition is just over a year old, and the firm has not published adoption metrics or performance data for the tools the Springbok team has built — making this the hardest of the three strategies to evaluate on results rather than intent.

Why Deal Structure Matters: S&C and LAER AI#

Sullivan & Cromwell tried a lighter-touch version of the same idea. Rather than acquiring outright, S&C made a minority investment in LAER AI, a Cornell Tech startup founded in 2018. LAER AI’s founders set up a lab inside S&C’s offices to develop AIDA (AI Discovery Assistant), a tool for automating first-level document review. S&C trained AIDA on dozens of past cases and deployed it on live matters. Partner Matthew Schwartz praised the tool’s performance publicly.

Then, in 2024, Epiq acquired LAER AI. The founders joined Epiq as vice presidents. The technology S&C helped develop became the Epiq AI Discovery Assistant — now available to any law firm willing to pay Epiq’s licensing fees. S&C remains a customer but no longer controls the technology it helped create. A minority stake didn’t give the firm control over the company’s corporate trajectory. When Epiq made an acquisition offer, S&C couldn’t block the deal. The IP, the team, and the roadmap all transferred to a third party. Cleary avoided this by acquiring Springbok outright. A&O Shearman avoided it by structuring a revenue-sharing arrangement that keeps both sides financially aligned. S&C’s approach cost the least upfront but delivered the least durable advantage.

Partner and Share the Revenue#

A&O Shearman co-develops AI products with Harvey and shares in the subscription revenue when those products are sold to other law firms and corporations.

The partnership dates to November 2022, when the legacy Allen & Overy became the first major law firm to deploy Harvey at an enterprise level. By the time the partnership was announced publicly in early 2023, roughly 3,500 lawyers had already submitted around 40,000 queries. Today, Harvey supports 4,000 staff across 43 jurisdictions. The firm and Harvey report that staff save an average of 2–3 hours per week on routine tasks like summarization, analysis, and translation. (These figures are self-reported by A&O Shearman and Harvey; no independent evaluation has been published.)

The latest phase of the collaboration, announced in early 2025, produced a suite of agentic AI tools that handle multi-step reasoning tasks: antitrust filing analysis, cybersecurity assessments, fund formation reviews, and leveraged loan documentation analysis. These tools will be sold to other law firms and corporate clients on a subscription or usage-fee basis, with A&O Shearman sharing in the revenue.

The collaboration has also produced ContractMatrix, a generative AI platform for contract drafting, review, and negotiation, built with Harvey and Microsoft and launched in 2023. Around 2,000 of A&O Shearman’s lawyers use ContractMatrix daily, and the firm reports it cuts contract review time by roughly 30%. Clients — including life sciences companies, financial institutions, and tech companies — license the tool for their own operations. Since launch, ContractMatrix has expanded through successive modules: Analyze for playbook-based review and Vantage for portfolio-scale analysis. Each builds on the institutional knowledge embedded in the last — the compounding pattern matters more than any single module.

Beyond Harvey, A&O Shearman runs Fuse, a legal tech incubator. The Financial Times named A&O Shearman the “World’s Most Innovative Law Firm” in 2025.

A proven product line. ContractMatrix is a daily-use tool for 2,000 lawyers with paying external clients. Three-plus years of enterprise deployment gives the firm knowledge about AI capabilities and limits that newer adopters can’t replicate quickly.

A new economic model. If the agentic tools and ContractMatrix licensing gain traction at scale, A&O Shearman earns revenue from other firms’ and clients’ use of tools built on its own lawyers’ knowledge — a fundamentally different model from hourly billing.

The risks are real. The partnership’s value is inseparable from Harvey. If Harvey gets acquired, pivots its strategy, raises prices, or fails to execute on its roadmap, A&O Shearman’s AI strategy is directly affected. And Harvey is now a platform in its own right: a $200 million round in March 2026 valued it at $11 billion, bringing total funding to roughly $1 billion. That cuts both ways — more runway to execute, but also more leverage to raise prices and more incentive to prioritize its own platform ambitions over any single firm’s. And selling AI-powered tools trained on your firm’s expertise to other firms raises a question partners will eventually ask: are we giving away our competitive advantage?

Freshfields: Wide with Many#

Where A&O Shearman went deep with one partner, Freshfields went wide with many. In April 2025, the firm partnered with Google Cloud to deploy Gemini across the firm. A year later, it announced a multi-year co-development deal with Anthropic, deploying Claude to all 5,700 employees across 33 offices. Within six weeks, adoption increased by approximately 500%.

The firm’s Freshfields Lab, co-led by partner Gerrit Beckhaus and staffed by legal professionals, software developers, and project managers, builds proprietary platforms — Dynamic Due Diligence, a Case Management Platform, a Multi-jurisdictional Insights Platform — that integrate whichever model performs best for the task. Chief Innovation Officer Gil Perez, who joined from Deutsche Bank in early 2024, described the approach as “tech-agnostic.”

The Anthropic partnership goes beyond licensing. Freshfields will serve as outside counsel for Anthropic, collaborating with Anthropic’s in-house legal team to define new AI-native workflows. Freshfields is also an early adopter and tester of Thomson Reuters’ next-generation CoCounsel Legal, rebuilt using Anthropic’s technology with Westlaw and Practical Law natively embedded.

One year into the Google partnership, over 5,000 professionals use AI tools built with Gemini. Over 2,100 regularly use Google’s NotebookLM Enterprise. Beckhaus told Law.com that Claude is “really good at nuanced reasoning” and “really good at drafting,” while Gemini excels in other areas — making the multi-model approach more than theoretical.

No single point of failure. If Anthropic raises prices or pivots, Freshfields still has Google (and vice versa). Best model for each task. Different models outperform on different tasks — the internal platforms route accordingly. But managing multiple strategic partnerships is operationally complex, and Perez acknowledged to the Global Legal Post that Freshfields could not yet estimate firm-wide ROI despite seeing significant benefits.

Subscribe and Build#

Cleary acquired. A&O Shearman and Freshfields co-developed. Most firms will do neither — they’ll subscribe to a platform and build on top. Latham & Watkins is the clearest example of what that looks like at scale.

For a firm that just wants a solid middle-of-the-road position, this is the lowest-risk path. You get production-grade capability immediately, add proprietary differentiation only where it pays off, and avoid the two biggest downside scenarios — sinking acquisition capital into a team that may not deliver, or tying your strategy to a partner whose roadmap you can’t control.

In August 2025, Latham signed an enterprise Harvey license covering research, drafting, and document review — the platform layer. On top of that, an internal AI strategy team led by Adam Ziegler builds practice-specific workflows that encode the firm’s own methodologies: how Latham’s M&A group structures due diligence checklists, how its finance practice reviews credit agreements, how its litigation teams organize discovery. The commercial platform handles what’s generic; the internal layer handles what’s proprietary.

The firm pairs this with institutional investment in AI fluency. A mandatory AI Academy trains over 400 associates per year, with billable credit for training time — a signal that AI adoption isn’t a side project.

Macfarlanes shows where the subscribe-and-build model leads. After achieving 80% internal adoption of Harvey, its Lawtech team built Amplify, a client-facing AI platform powered by Harvey’s API — clients use it without needing a Harvey license themselves. The internal layer turns the firm’s institutional knowledge — playbooks, precedent libraries, partner expertise — into a RAG pipeline connected to the firm’s document management system.

Lower barrier to entry. A team of 2–5 engineers can stand up this kind of system. No acquisition, no multi-year co-development negotiation. The 2026 Thomson Reuters/Georgetown State of the Legal Market report found that legal tech spending grew 9.7% in 2025, the fastest rate ever recorded, and most of that spending went to vendor subscriptions.

The risk is the seam. If the commercial platform and internal tools don’t share context, lawyers toggle between systems and the value drops.

Harvey is now moving to close that seam itself. In May 2026 it launched a Command Center for managing enterprise AI adoption and partnered with DeepJudge to connect a firm’s institutional knowledge directly to the platform — pushing into the proprietary internal layer that subscribe-and-build firms built to differentiate. [Medium confidence] As platforms absorb the knowledge-integration layer (Harvey’s Command Center and DeepJudge deal are the first convergent signals), the “build” half of subscribe-and-build shifts from engineering toward configuration — narrowing the gap a small internal team can open over a firm that only subscribes.

The Trade-Offs#

| Acquire | Partner | Subscribe + Build | |

|---|---|---|---|

| You own | The team, the IP, the roadmap | The product line, the revenue share | The internal workflows, the playbook layer |

| You risk | Culture clash, maintenance burden, no outside feedback loop | Partner dependency, giving away expertise | Vendor lock-in as a customer, not a partner |

| You need | Acquisition capital, retention strategy for technologists | Deep subject-matter expertise worth productizing | 2–5 engineers and a training program |

| Best for | Firms that want full control and can sustain engineering investment | Firms with institutional knowledge worth monetizing | Firms that want speed and can build differentiation on top |

What to Watch#

Does Cleary’s team ship results? The acquisition is over a year old with no public data on adoption or performance. If the AI Acceleration team builds tools that measurably improve practice-group output, every large firm will re-evaluate whether to acquire rather than license. If it stalls, the acquisition becomes a cautionary tale about integrating technologists into a partnership structure.

Can A&O Shearman and Freshfields sustain their partnerships as the market shifts? The co-development model works when both sides are aligned. If Harvey raises prices, gets acquired, or pivots to competing with its law firm partners, the partnership’s value changes overnight. Freshfields’ multi-vendor approach hedges this risk but creates operational complexity.

Does subscribe-and-build become the default? Latham’s model requires the least upfront commitment and the most common resources (a platform license and a small engineering team). If it produces comparable output quality to deeper strategies, the acquire and partner models become harder to justify — especially for firms outside the top 20.

Further Reading#

- Cleary Gottlieb Acquires Springbok AI. Cleary’s acquisition announcement (March 2025).

- A&O Shearman and Harvey Agentic AI Agents. The co-development and revenue-sharing announcement.

- A&O Shearman AI Strategy Analysis. Klover.ai deep dive on the Harvey partnership.

- Freshfields and Anthropic Multi-Year Collaboration. The Anthropic partnership announcement.

- Freshfields Reports Google Cloud Collaboration Delivering Transformation at Scale. One-year Google Cloud results.

- Freshfields Now Partners with Anthropic. Artificial Lawyer’s analysis.

- Epiq AI Discovery Assistant. How S&C’s LAER AI investment became Epiq’s product.

- Harvey Announces Firmwide AI Deployment for Latham & Watkins. The enterprise Harvey license.

- Legal Tech Spending Surges 9.7%. 2026 Report on the State of the US Legal Market.

- ABA Journal: Cleary’s “Extremely Rare” Move. ABA coverage of the Springbok deal.

This post is part of the Law Firm AI Positioning series on LegalRealist AI. It is intended for informational and educational purposes only and does not constitute legal advice. AI capabilities, strategies, and market conditions described here reflect publicly available information as of the publication date and are subject to rapid change.

{kind=link}

{kind=link}

{kind=link}